What's 🔥 in Enterprise IT/VC #354

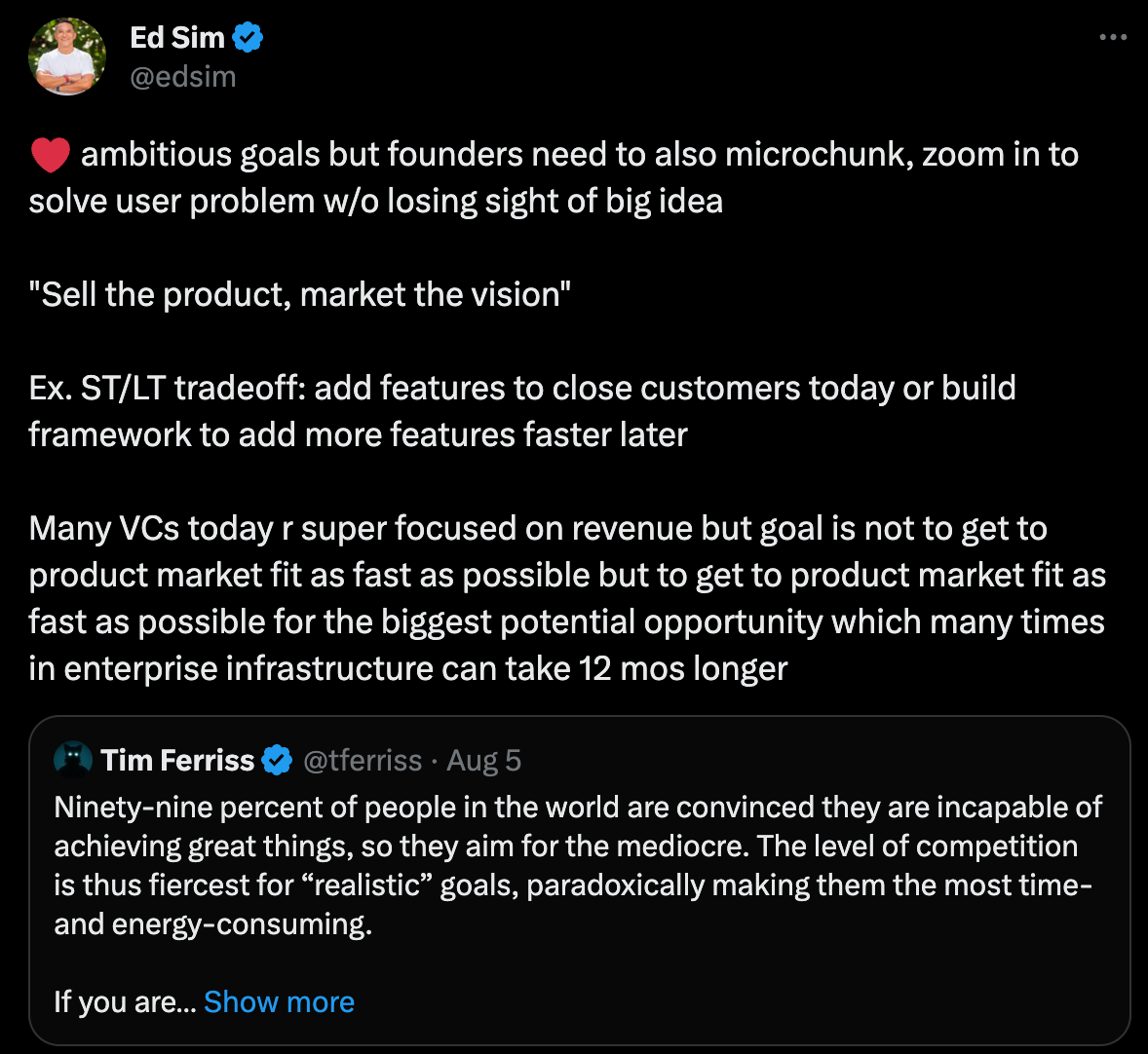

On huge ambitions in today's venture market vs. what investors are telling you now

Just a reminder that VC is a hits driven business and only a rare few financings, <3% realize a >20x return. In addition, almost 1/2 of financings result in <1x (more from Correlation here)

This is why every investment that is made by early stage venture capitalists has to have the potential to realize an enormous outcome as the outliers are the primary driver of returns.

That being said, I know of a number of founders who are feeling whiplash from investors as of late. On the one hand, investors want super big and ambitious ideas and on the other hand, they want founders to get to revenue now in order for them to write a check. In a perfect world, one can do both, but for super early stage startups, the more revenue you go after means that you may sacrifice LT product build which can cement an even bigger future. This is especially true for enterprise infrastructure companies as these can take a bit longer to bake and mature. The goal is not to get to product market fit as fast as possible but to get to product market fit as fast as possible for the biggest potential opportunity.

Along those lines, here’s some commentary I have around Tim Ferriss’ “think super big” post which I fully endorse but with a caveat.

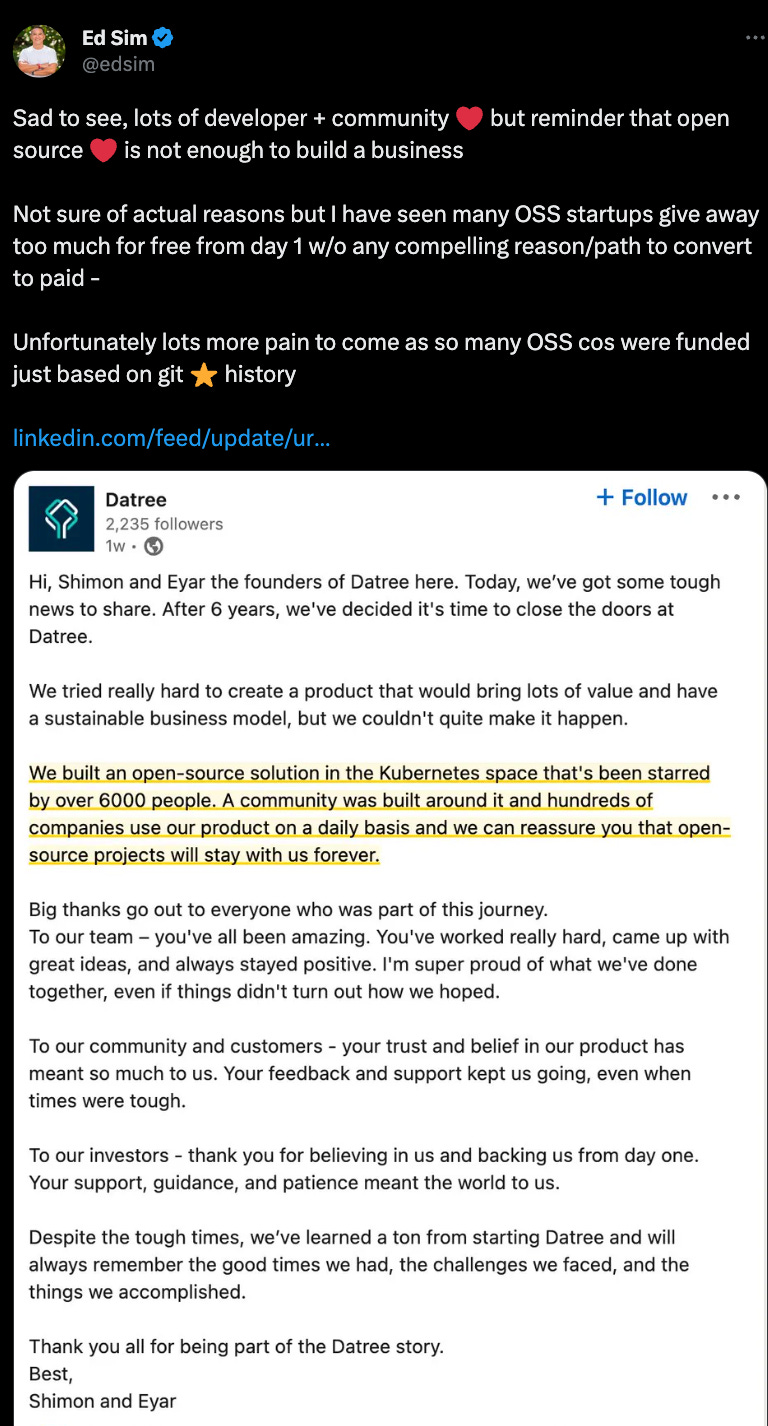

When thinking ambitiously, many infrastructure founders think that going open source is the recipe for success. The tailwinds one can get from a community of developers writing code and building and enhancing your product along with the marketing tailwinds can help propel many a startup to success. However, I can tell you that what happened to Datree below is a conversation I’ve had with many other OSS related founders and investors who have lamented how hard it is to get new financing rounds done, even with good usage. The problem is that, to my earlier point, investors want more revenue now to fund a startup and in open source - it’s tough to build a business, especially if you give away too much for free.

The point is one needs to be quite intentional about why they want to open source software and clearly think well beforehand what an upgrade path would look like and why. Sadly there are lots of companies who did not think as thoughtfully about this and there will much more carnage to come in OSS land.

To that end, it’s no surprise that Hashicorp changed its Open Source license terms to the Business Source License (BSL) which is still open source but prevents vendors from bundling existing Hashicorp OSS sponsored projects and reselling them (from Runtime).

For its part, HashiCorp simply grew tired of companies that are making money through services that rely on its open-source projects, said Armon Dadgar, the company's co-founder and CTO, in an exclusive interview with Runtime.

"Given the sort of capitalistic incentives these other companies have, I don't think asking them politely is going to change their behavior," Dadgar said.

Dadgar argued that for almost all users of that code, nothing really changes. And he believes that keeping the source code available, as opposed to completely closing it off, provides operational and security benefits for users, which Redmonk's O'Grady seconded.

But there are obviously commercial motivations behind HashiCorp's decision, with revenue growth declining over a rough 12-month period for enterprise tech in general and its stock down 67% since its 2021 IPO.

"If your competitors are commercializing your IP, you either stop giving it to them by not making it open, or you stop giving it to them by changing your license," Dadgar said. "We're not the first and we're not the last (to make this move). And I think that trend is going to continue; there's this sort of fundamental problem that sits at the heart of open source, which is there's a bit of a tragedy of the commons here."

This is really huge news as Hashicorp was built off back of community and also many ISVs who integrated with some of these projects. I totally understand the need for these companies to make 💰 as evidenced by the above announcement of another OSS-based company shutting down, but longer term what does open source really mean when sponsored by a single vendor? This is something to watch in the coming weeks, and I’ll report back as I learn more.

As always, 🙏🏼 for reading and please share with your friends and colleagues.

Scaling Startups

Must read covering how some of the best enterprise startups came up with their idea including Databricks, Gong and some of our own like Snyk and Front. As readers of What’s 🔥 know, I’m quite biased towards learning from past pain with deep domain experience but plenty of amazing startups were built without any prior deep knowledge in a space.

Cathy Gao from Sapphire Ventures shares what it takes to raise a Series B 🧵

Read comments to see who is still remote first as Zoom, the biggest beneficiary of COVID, wants employees back in the office

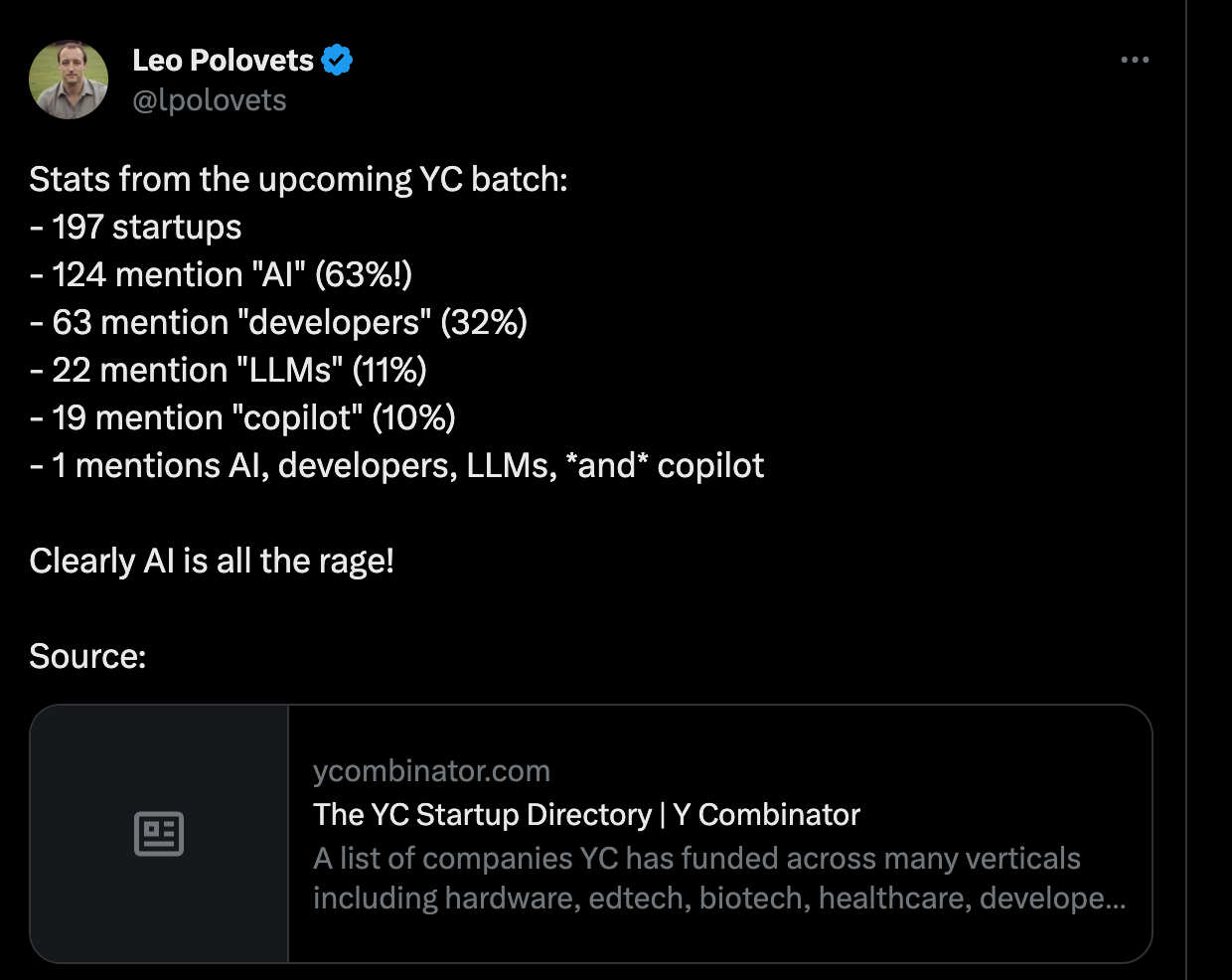

AI and Dev tools are flavor of month at new YC batch

Enterprise Tech

The Cloud 100, Forbes list of the world’s best private cloud computing companies is back - a number of AI companies appeared on this year’s list with OpenAI debuting at #1, 4 cybser security cos are in the Top 20 with Tanium, Netskope, Wiz and Snyk (a portfolio co) and a few OSS cos like Databricks and Grafana in Top 20

Black Hat, the second largest cyber security conference, just concluded and here’s a list of Top 10 startups

📉 Datadog took a massive 17% hit to stock price after announcing earnings with much slower growth ahead where Q4 will grow 15% YoY vs. its previous forecast of 23% growth! More importantly the days of Best in Class NDR (Net Dollar Retention) > 130% are over. Company indicated that it is at 120% now but with current trending will be below 120% next quarter. This has huge implications for many financial models

Meanwhile, we are seeing some churn of smaller customers who have limited impact on our revenues. As a result, our gross revenue retention rate remains unchanged in the mid to high 90s, indicating the stickiness of our product and the importance of our product to our customers' operations. We are executing on strong new logo bookings and new customers contributing meaningfully to our growth as they ramp up. As Olivier mentioned, we had our second largest new logo bookings quarter and a record for Q2.

We expect these customers to become more meaningful as they expand with us. In Q2, about 40% of our year-over-year revenue growth, or 10 points of growth, was attributable to growth from these new customers that were acquired in the past year. Finally, we continue to see consolidation opportunities, particularly in larger deals. Consolidation allows our customers to improve functionality by getting all of their data into one platform while saving money at the same time.

Moving on to our trailing 12-month dollar-based net retention rate or NRR. NRR was over 120% in Q2 as customers increased their usage and adopted more products. As we expected and as we discussed on last quarter's call, our trailing 12-month NRR declined but was above 120 in Q2 as existing customers continue to scrutinize their tech stack costs and make efficiency improvements. If our growth trajectory continues at current levels, we expect our trailing 12-month NRR to decline to below 120 in Q3.

Here’s my commentary from February indicating what new best in class NDR will be and why:

What's 🔥 in Enterprise IT/VC #329

·

Datadog is one of the best executing software infrastructure companies having grown 63% YoY to $1.68B of Revenue in 2022. Q4 was also strong clocking in at $469.4M of Revenue but a YoY growth rate of 44%. While these numbers are fantastic, the decelerating growth in Q4 is certainly an area of concern. Such that management guided down its 2023 growth for…

👀 Tome, AI presentation creator at $2M ARR run rate looking to raise at eye popping $600M valuation (The Information)

Tome, founded in 2020 by Keith Peiris and Henri Liriani, both former managers at Meta Platforms, designs presentations using AI and simple text prompts. After launching its product last year, Tome started charging users for added services in April. It charges $8- $10 a month for Pro users and offers pricing options for enterprise users. A majority of Tome’s over 10 million users use the product for free, according to a person with direct knowledge.

The 60-person startup recently told potential investors it has passed a $2 million annual run rate, a measure that takes a recent period’s revenue and multiplies it over a whole year, according to a person with knowledge of its finances. So far, Tome raised a total of $81 million from investors including Coatue Management, Greylock Partners and 8VC. Its most recent deal valued it at $300 million, according to Forbes.

Enterprise sales is hard - here are performance numbers for Cloudflare sales reps, cost to generate new $$$ super expensive when only 1/3 reps at quota

Yes, we have way too many plug-ins clogging up IDEs…

AI Is Generating Security Risks Faster Than Companies Can Keep Up? (WSJ) - great to see port co Protect AI sharing why enterprises need ML BOMs (bill of materials) to secure its AI

Interest in generative AI has created an opening for startups like Protect AI, which aims to help businesses track the components of their homegrown AI systems through a platform it calls a “machine-learning bill of materials.” The company said its platform can also identify security policy violations and malicious code injection attacks.

The Seattle-based startup recently found a vulnerability in the popular open-source machine-learning tool MLflow, which could have allowed an attacker to take over a company’s cloud account credentials and access training data, said Protect AI co-founder and President Daryan “D” Dehghanpisheh.

Those types of attacks—plus new forms like “prompt injections,” where hackers use “prompts” or text-based instructions to manipulate generative AI systems into sharing sensitive information—all represent AI-based supply chain risks that CIOs need to account for, Dehghanpisheh said.

Though rapid growth in generative AI has given rise to a plethora of new tools and AI models, most companies are still trying to get a full view into their data, code and AI operations, said Protect AI co-founder and CEO Ian Swanson.

Some companies still making money in crypto - Circle generated $219M in adjusted EBITDA in first half of 2023

Markets

👇🏼💯 must read 🧵 from Bill Gurley on why “dry powder” isn’ magically going to get deployed…

You can frequently read articles referencing VC "dry powder" and inferring that these large dollar amounts are "burning a hole" in someone's pocket & will imminently find their way to the market. I totally understand the assumption, but things don't really work this way. [cont]

😢 📉 Discount 🦄: Check Point pays $490 million for Perimeter 81, one year after being valued at $1 billion

Check Point has acquired Israel's Perimeter 81 for $490 million, marking its second-largest purchase in company history. This valuation could be considered as disappointing for Perimeter 81 as it was valued at $1 billion in its most recent funding round in 2022, raising $100 million in a Series C. Nevertheless, some investors, including Spring Ventures, listed on the Tel Aviv Stock Exchange, will net a generous profit from this sale.

Data security is 🔥 as Laminar out of Israel bought by Rubrik for reported $100M