What's 🔥 in Enterprise IT/VC #329

Where will best in class Net $ Retention land in 2023?

Datadog is one of the best executing software infrastructure companies having grown 63% YoY to $1.68B of Revenue in 2022. Q4 was also strong clocking in at $469.4M of Revenue but a YoY growth rate of 44%. While these numbers are fantastic, the decelerating growth in Q4 is certainly an area of concern. Such that management guided down its 2023 growth forecast to 23% - yes 23% YoY to $2.07B. Folks that’s a steep drop from 63% growth and reflective of the IT spending environment we live in today. Let’s dig deeper.

Here’s Olivier Pomel, Co-Founder and CEO

And our dollar-based net retention rate continued to be over 130% as customers increased their usage and adopted more product. Our platform strategy continues to resonate in the market. As of the end of Q4, 81% of customers were using two or more products, up from 78% a year ago; 42% percent of customers were using four or more products, up from 33% a year ago; and 18% of our customers were using six or more products, up from 10% last year. Now, moving on to this quarter's business drivers.

Overall, we observed slower user growth with existing customers, while continuing to scale on new logo acquisition and new product cross-sales. Starting with usage. Usage growth of existing customers in Q4 was overall slightly lower than what we observed in Q2 and Q3, which we attribute, first, to a continuation of cloud cost optimization by our larger-spending customers; and second, to a seasonal annual slowdown in the second half of December that was more pronounced than in previous years. As in Q2 and Q3, we continue to see more optimization from customers with a larger cloud footprint, while our smaller-spending customers are exhibiting higher growth.

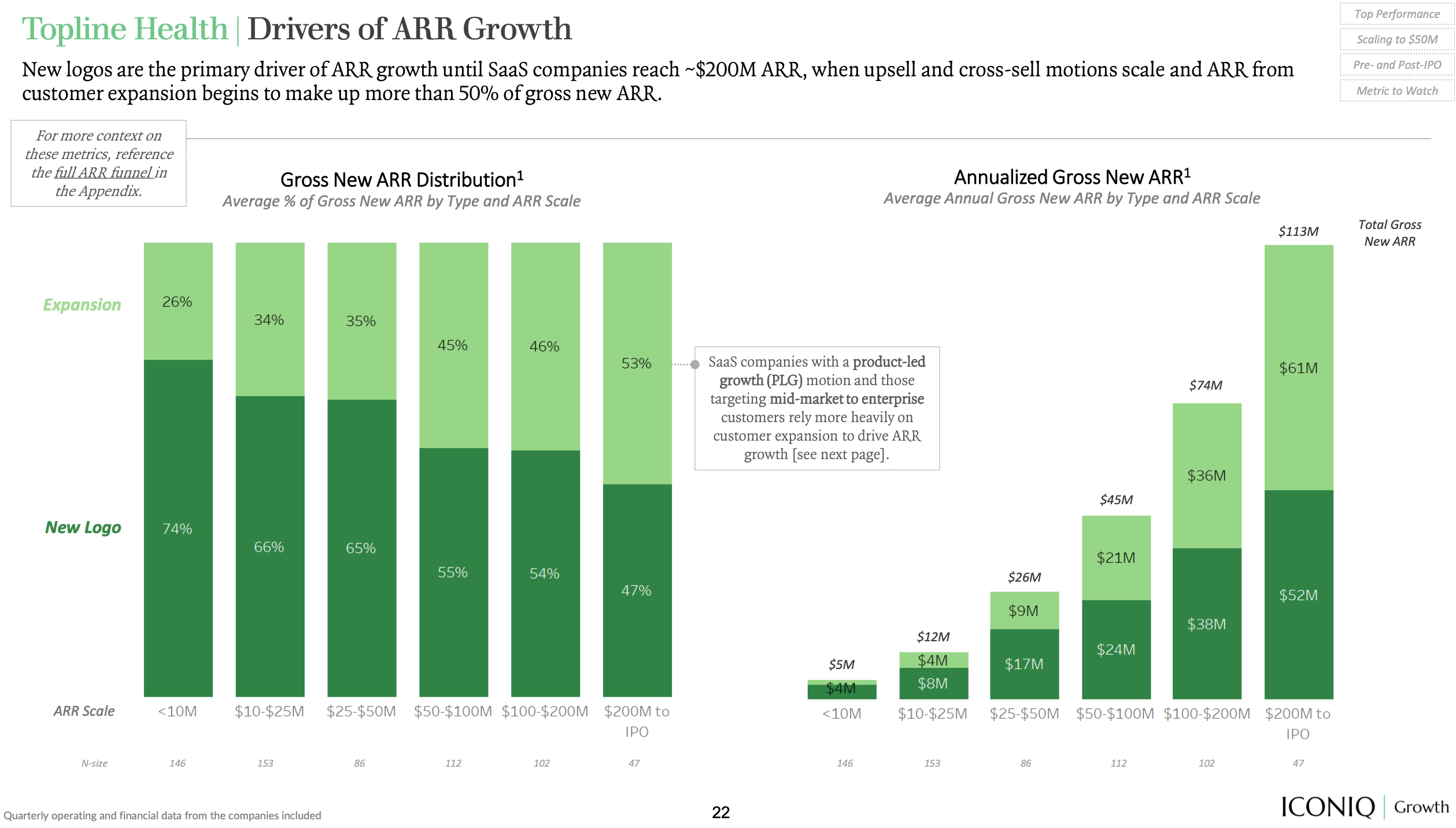

It’s clear that Datadog’s multi-product portfolio has been keeping the NDR >130% but there are signs of this not lasting as customer usage 📉. It’s been an absolute rule for the last couple of years that the BEST enterprise software companies have a Net $ Retention > 130%. It’s been the case for the last two years, and many still consider that to be a universal truth. In fact it is one of the most amazing and efficient growth engines as you can see from this chart from Iconiq - as companies scale, the breakdown of New ARR from expansion of existing customers is close to 50% for companies >$50M ARR. While Datadog does not explicitly discuss NDR numbers for its lower growth forecast, it’s pretty clear that’s a huge reason for the forecasted lower growth in 2023.

When finally asked directly about NDR, here’s Dave Obstler‘s (CFO) answer:

Implicit in that guide is below 130% NDR.

Matt Hedberg -- RBC Capital Markets -- Analyst

OK. Thanks. And then, maybe just, David, on the guide, obviously with kind of a mid 20s revenue guide. You talked in the prepared remarks about having an NRR above 130% for almost two years.

You know, presumably that dips below 130%. Any sort of commentary on how that might progress through the year?

David Obstler -- Chief Financial Officer

Yes. I think you're right. Implicit in that guide is below 130%. We'll report to everybody as we have that.

You know, we've seen it relate to a decel, I would say, on that, that given the change in the organic growth rate that we've been talking about starting in the middle of Q2 last year. It would be -- it's getting past that to the extent that it changes -- that changes that net retention, plus or minus, given the net retention is comparison against the year-on-year customers. So, you do have headwinds in the compare through the time that we had the change of the organic, which we had said was in the middle of Q2 of last year.

While Datadog is just one data point on infrastructure, it’s an important one given its market share, success, and breadth of products. While not an infra company, here’s Monday.com trending lower as well.

Here’s Twilio

As you plan your sales models and forecasts for 2023, I’d take a harder look at what NDR numbers you’re benchmarking against as it seems to me that while Datadog hit it’s 130% NDR number, it’s going to fall this year, and it’s just the beginning of a new normal for best in class which will likely land in the 115-120% range, save a few outliers. As a startup who is modeling against some of these public comps, don’t fret as these public cos are reporting a few months behind, and I can promise you that the >130%+ NDR days are over. You are probably still best in class when the dust settles in the next few months. Just keep building, fighting the good fight, and protect that customer base.

As always, 🙏🏼 for reading and please share with your friends and colleagues.

Scaling Startups

Want more growth? Here are 3 ways…

Lenny Rachitsky@lennysanWhat precedes an inflection in growth? I researched 20+ products and found a few surprises: 1. The majority of growth inflections came after a specific product improvement 2. Many growth inflections came from an unexpected external event, without the product changing at all...

Lenny Rachitsky@lennysanWhat precedes an inflection in growth? I researched 20+ products and found a few surprises: 1. The majority of growth inflections came after a specific product improvement 2. Many growth inflections came from an unexpected external event, without the product changing at all... 4:16 PM · Feb 14, 2023122 Reposts · 930 Likes

4:16 PM · Feb 14, 2023122 Reposts · 930 LikesUnderstanding the maze of customer contracts with Jake Stein and Common Paper (a portfolio co) from design partner to first sale…

Ed Sim@edsim👇🏼 for founders closing their first contract... get them to sign on the line that is dotted but which one? @jakestein breaks it down and has a standard contract for very situation @UseCommonPaper Jake Stein @jakestein(1/2) I talk to a lot of founders who are confused by the alphabet soup of SaaS contracts - NDAs, SLAs, DPAs, etc. They're focused on closing their first customers, and they know they are supposed to get a contract in place, but they don't have any context on what to use.6:15 PM · Feb 14, 20231 Like

Jake Stein @jakestein(1/2) I talk to a lot of founders who are confused by the alphabet soup of SaaS contracts - NDAs, SLAs, DPAs, etc. They're focused on closing their first customers, and they know they are supposed to get a contract in place, but they don't have any context on what to use.6:15 PM · Feb 14, 20231 Like

Enterprise Tech

💪🏼 “Beyond Silicon Valley, Spending on Technology Is Resilient” NY Times

Ed Sim@edsim👇🏼 good reminder on IT spend from @nytimes - so many non-tech cos had such a hard time hiring engineers last 2 yrs but not any more - many still hiring and building new software which means they need more developer tools + infra to keep building nytimes.com/2023/02/13/tec…… https://t.co/aSri3TF8Mw2:09 PM · Feb 13, 202319 LikesReplit journey from 0 to 20M developers - package mgr to cloud based IDE to it’s own co-pilot like features

Amjad Masad ⠕@amasadReplit has exceeded 20 million developers on the platform. Especially proud of how we’re expanding what it means to be a developer: it’s not just engineers that are using Replit, but also marketers, solopreneurs, scientists, students — and so many more! blog.replit.com/20-million-dev… 10:08 PM · Feb 16, 202342 Reposts · 634 Likes

10:08 PM · Feb 16, 202342 Reposts · 634 LikesPlatform engineering at Palo Alto Networks with developer portals - great overview of the breadth and depth of what OSS project Backstage provides

Another incumbent rolling out GPT features to a large installed base - this from CEO of ZoomInfo 🧵

Henry Schuck@HenryLSchuckGenerative AI is the future of software, and today I’m thrilled to announce that @ZoomInfo will incorporate GPT technology across our go-to-market platform.7:26 PM · Feb 16, 202316 Reposts · 196 Likes2 people and 4-5 months to get the first holy shit moment…and then exploded internally to 400-500 users with 65% retention after 30 days and with a crappy, intensive UI

swyx 🤖@swyxWatching @natfriedman tell the story of hammering out the @github Copilot UX with @alexgraveley’s tiny team They knew it was going to be a success when, in internal trials, the lifetime retention rate was >65% 🤯 (at the @heyjasperai conf)12:08 AM · Feb 15, 20232 Reposts · 127 Likes🤯 Whopper of a seed round for developer first auth play/security co Descope - I get it, repeat founders who sold Demisto to Palo Alto but wow…and from Security Week - that’s quite a burn if this is going to last 24-36 months

He said the $53 million seed round, which was led by Lightspeed Venture Partners and GGV Capital, gives the Descope team a 24-36 month runway to bring its new platform to market.

👇🏼 must read 🧵

Dave Kellogg@KellblogHow much does it cost to grow from $20M to $100M. Some quick back-of-the-envelope math. A thread 🧵6:37 PM · Feb 14, 202332 Reposts · 279 LikesHackers been on ChatGPT for awhile - here’s more from Checkpoint Research on how hackers in Russia using it to create phishing emails and more…scary stuff for sure

Justine Moore@venturetwinsAs ChatGPT becomes more restrictive, Reddit users have been jailbreaking it with a prompt called DAN (Do Anything Now). They're on version 5.0 now, which includes a token-based system that punishes the model for refusing to answer questions. 2:41 PM · Feb 5, 20233.11K Reposts · 21.6K Likes

2:41 PM · Feb 5, 20233.11K Reposts · 21.6K Likes🤯

Ian Miles Cheong@stillgrayThis is not real. This was produced in Unreal Engine 5.7:25 AM · Feb 11, 20232.64K Reposts · 25.1K Likes

Markets

All 👀 on Stripe and Databricks to unlock a non-existing IPO market but The Information tells a story of slowing growth

The pitch includes more sobering numbers about Stripe’s past year. Stripe’s gross revenue was $14.3 billion last year, up 27% from the prior year. That represented a slowdown from 60% growth from 2020 to 2021. Stripe said a net revenue figure called “transaction margin before losses” sat at $3.2 billion, up 25% from the previous year.

The Information previously reported that Stripe burned through more than $500 million of cash last year as its revenue growth rate fell sharply. A net revenue figure that takes into account fraud-related losses came in at about $2.8 billion, The Information has reported, representing growth of about 18%.

Crunchbase January venture funding data out

Meanwhile, seed and early-stage funding were down by more than 45% year over year. Seed was up 14% and early stage down 7% month over month.

Stripe timed its needs for both employee liquidity and external cash for operations pretty badly. A lot of employees would have been much better off if they made moves a year or 18 months ago.

Now they’re getting diluted when the company needs to raise at a lower price tag and having to sell for less in opaque secondary markets