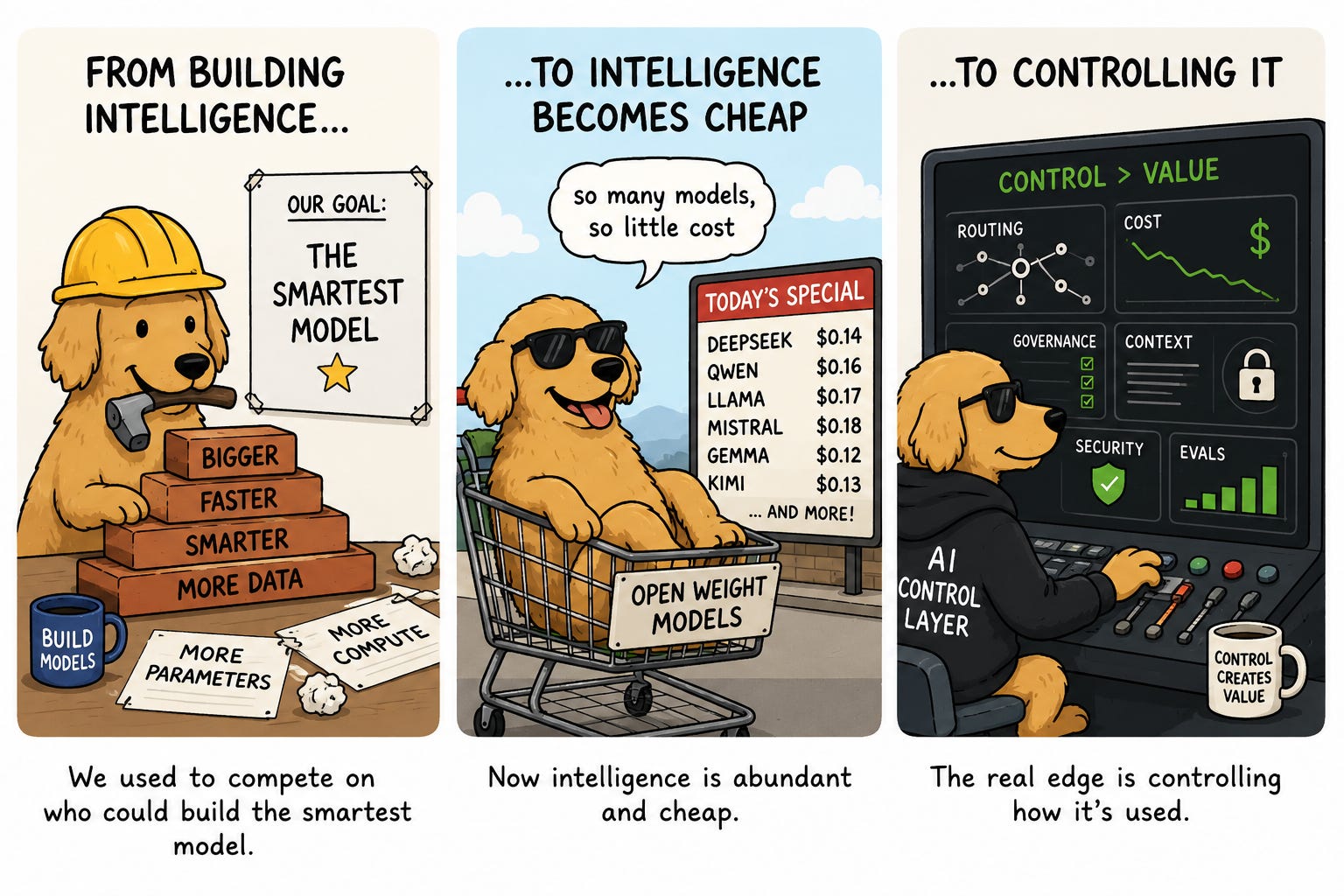

Over the past year I’ve argued that AI models would become abundant while the value would shift to the software that sits above them. This week may have been the clearest evidence yet that we’re entering that world.

This wasn’t really a story about China. It wasn’t really a story about OpenAI. And it wasn’t just another story about cheaper models.

It was the week the market began pricing intelligence like a commodity.

As you know I’ve been long open weight/open source models for quite a long time, and I feel like the great reckoning is accelerating. Everyone always wants frontier lab state-of-the-art (SOTA) models if they can, but once subsidization ends, and other alternatives become good enough and dramatically cheaper, economics begin to win.

Brian Armstrong just described how Coinbase has cut AI spend nearly in half while token usage continues to grow. They did it with better defaults, intelligent routing, caching, leaner context, and visibility. They’re no longer optimizing for the smartest model but for maximum intelligence per dollar.

This is what every technology market looks like when it begins to commoditize: buyers stop asking for the absolute best product and start optimizing for cost, flexibility, and control.

Another example among many is Hugging Face which is the largest hoster of open source models and infra just crossed $100M of ARR with recent growth by…you guessed it - Chinese models.

None of this would matter if open weight/open source models weren’t good enough and much cheaper. Per JPM:

Many tokens consumed in the future may not come from frontier models but from smaller open models that are up to the tasks. Amazon now offers a half-dozen open models at a fraction of frontier pricing, and NVIDIA is teaming up with Dell, Lenovo and HP to make PCs designed with AI agents.

This doesn’t mean frontier models don’t matter. They absolutely do. But most enterprise workloads don’t require frontier intelligence every time. They require the right intelligence at the right cost, delivered securely, with the flexibility to switch models as economics, performance, and policy change.

Whether by building on frontier models or through alleged distillation, the gap continues to compress.

Another consequence may be increasing government involvement in access to frontier models. The U.S. government now will decide who gets access to the latest model releases and when 🤯. This will further separate the world of the “haves” versus “have nots” and also allow China to catch up very quickly and close that 9 month gap between best in class and free.

The bigger risk isn’t just geopolitics. It’s a future where access to the most capable models becomes increasingly restricted while open models continue improving. That only strengthens the case for enterprises to own more of their AI stack.

In the meantime, enjoy access to cheaper intelligence and make sure you get your multimodel AI workflow strategy rolling. This all builds on what I laid out in What’s 🔥 #502 two weeks ago. Re-upping it here.

Satya Nadella recently offered a framework that I think nails where the value is heading. He argued that a company’s private evals may ultimately become its most valuable IP. (h/t to Gokul for summarizing this)

Satya described where value accrues, while Brian Armstrong is showing how enterprises will operate.

The good news is that only 8% of enterprises have broadly deployed AI agents today (UBS), so we’re still in the early innings. Even if intelligence keeps getting cheaper, enterprises will deploy exponentially more agents. Coding agents consume enormous numbers of tokens. Multimodal AI expands compute requirements. Demand for intelligence keeps growing even as the price per unit falls.

The frontier labs may face pricing pressure. Everyone building above them won’t.

The first era of AI was about building intelligence.

The second era of AI isn’t about building smarter models; it’s about controlling intelligence through routing, governance, security, cost optimization, private context, and private evals, which together become the operating system of enterprise AI.

In a world where intelligence becomes abundant, control compounds.

As always, 🙏🏼 for reading and please share with your friends and colleagues!

Thanks for reading What's Hot 🔥 in Enterprise IT/VC! This post is public so feel free to share it.

#the model routing wars continue as Sakana releases a single model API which claims it matches the performance of Fable and Mythos 🤔 - great marketing but some real questions raised by Elie 👇🏼

the biggest and most obvious issue is that they are introducing a “test time scaling” method with “best of N” over models, and they literally NEVER REPORT the number of output tokens or cost to achieve a benchmark/task

#fun time continuing our conversation from the McKinsey Tech Leadership Forum workshop with leading enterprise CTOs/Heads of AI on where are we with diffusion of agentic workflows and what’s ahead

#what used to be mostly a “buy data from vendors” game has shifted toward “build sophisticated internal research infrastructure” because the data/reward design itself is now a core research problem and everyone needs to own their evals

#speaking of, here’s why we’re so excited about Generalist AI, a boldstart port co - this demo was not possible a few years ago - variables changing and the arm adapting

#speaking of other tokens, the tokenization of real-world assets is happening

The tokenized real-world asset market has grown to nearly $32 billion, highlighting increasing institutional adoption of blockchain-based asset infrastructure.US Treasuries (47%) and private credit (19%) account for approximately 66% of the market, emerging as the dominant use cases for asset tokenization. (Apollo)

Markets

#SpaceX and now Anduril rewriting the rules for venture scale outcomes