So many lessons learned from Cursor’s meteoric rise and sale to SpaceX for $60 billion which became official this week. There are so many founders who tinker, tinker and tinker trying to create perfect in their own minds, but don’t get out there fast enough to test their story.

Lesson 1 of many: just ship it and learn and iterate or kill. That is it - you need to know what real signal is from noise. Here’s how many different ideas or products that Michael initially ran through.

Anyhow…Cursor’s success isn’t just a story about coding.

It’s a story about where value accrues in a world of abundant intelligence. For years, the assumption was that the winners in AI would be whoever built the biggest and best models. This week provided more evidence that the future may be far more complicated.

Open source keeps getting better. Chinese models continue to close the gap. Enterprises are increasingly embracing a multi-model world. And startups are building massive businesses by owning the workflow, the data, the evals, and the customer relationship.

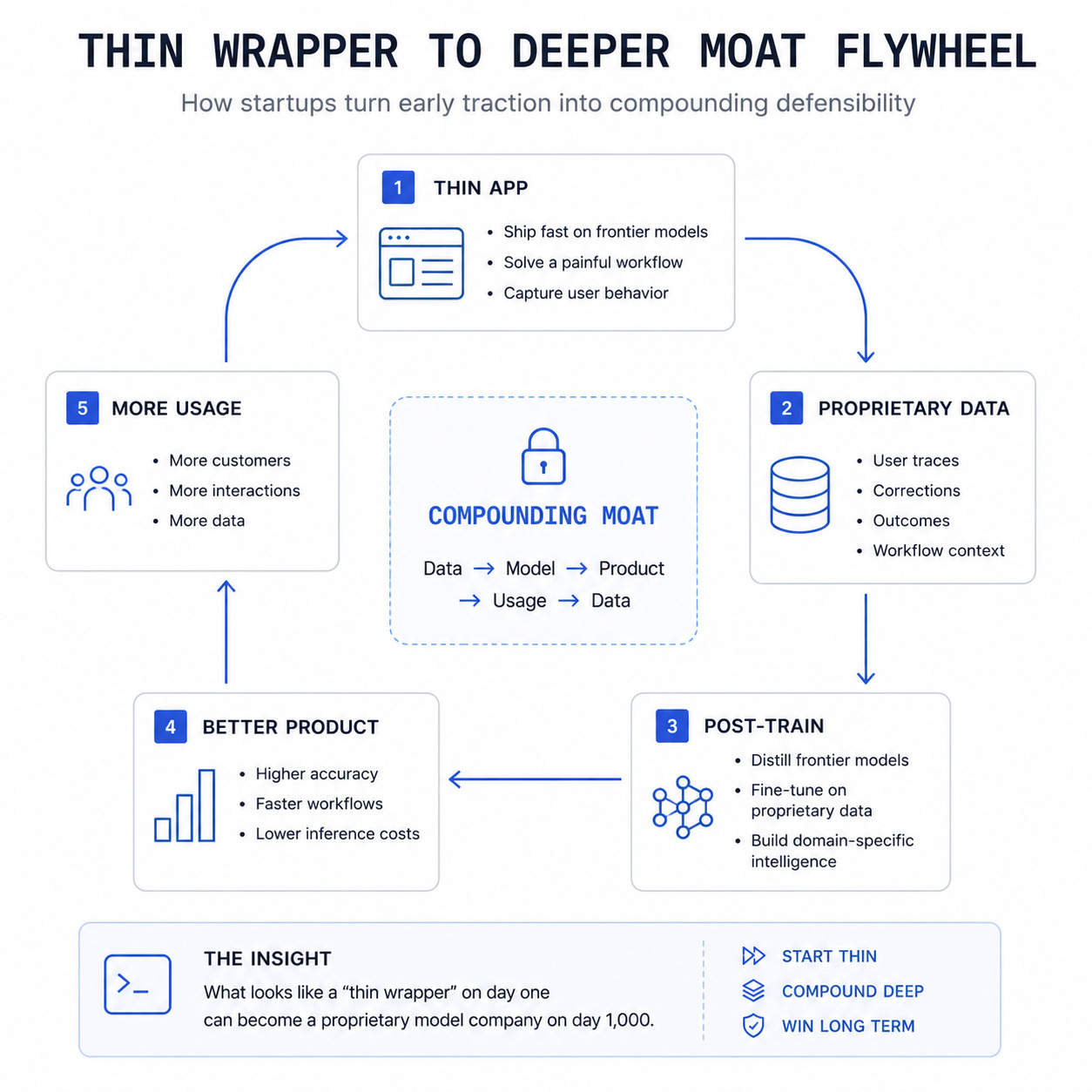

And when intelligence is abundant, the model stops being the moat. The flywheel becomes the moat.

Own the workflow, and you capture the data. Capture the data, and you can post-train your own model. Better model, better product. Better product, more workflow. More workflow, more data.

Whoever spins that flywheel fastest wins. And they can do it at any layer.

This week felt like a major acceleration of that trend.

A year ago most people would have laughed at the idea that an open-source Chinese model could be mentioned alongside the leading frontier models. Not anymore.

This is about far more than a leaderboard. It’s another reminder that model quality continues to converge. Which means intelligence itself is becoming more abundant.

This is also why model infra companies like Baseten continue to raise at insane growth numbers

Baseten, which specializes in providing software and computing capacity to companies tapping in to lower-cost AI models, is finalizing a $1.5 billion fundraising round. It will be a dual-tiered structure, with some investors putting in money at an $11 billion valuation and others at a $13 billion valuation, according to Baseten.

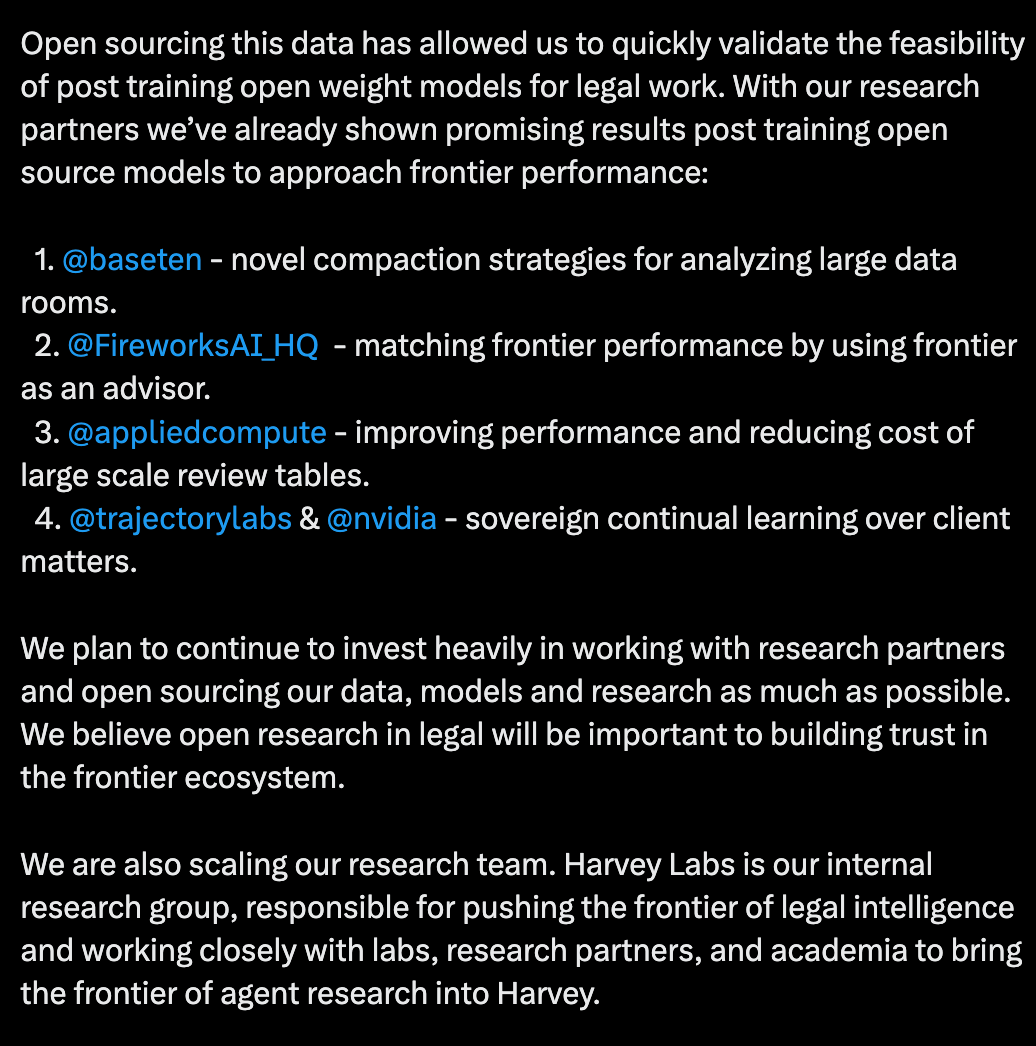

Which makes sense considering that $11B startups like legal AI co Harvey is doing hard core model post-training sitting on top of this stack.

Here’s the full post on Harvey’s strategy laid out by Gabe.

Finally, the DeepSeek moment is here, potentially, for Microsoft. Whether or not Microsoft offers, even the idea of it, shows how far we have come (Axios)

The cat is out of the bag - we are all living in a multi-model world and its only accelerating. The conversation used to be can anyone catch Claude and now it’s how many models should we use.

Cursor didn’t stop at owning the workflow. They used it to capture the data, then turned the data into their own model. Harvey is running the same loop in legal. The app layer reaching back down to the model layer isn’t a complication. It’s just the flywheel completing a full rotation.

Now look at the full Michael arc.

Start with a pile of ideas. Kill most of them. Build an IDE. An insane bet. Launch Cursor. Subsidize insane growth on negative gross margins.

Survive an assault from your own partner, Anthropic and Claude Code.

Post train your own model on Chinese open source Kimi. Sell to SpaceX. Take that data flywheel and point it at unlimited compute. And lo and behold, launch your own model at Anthropic and OpenAI scale.

Defense/Hardware: 9 Mothers (counter-drone robots, $1.6M in sales, ~$200M valuation, potentially highest-valued in YC history). Dispatch (return vehicles for space manufacturing). Physical AI is real.

AI Code Infrastructure: Arga Labs (digital twin sandboxes for testing AI-generated code), Sazabi (find + auto-fix production bugs), Superset (run 100+ coding agents simultaneously). Your “second wave” thesis everywhere. More code = more testing, more debugging, more orchestration.

AI Security: Silmaril (agent prompt injection defense, autonomous threat probing). Directly in your Keycard/Surf AI orbit.

Non-technical builders: Lightsprint (PMs ship features without engineers), Ploy ($27M seed from First Round, Webflow CTO’s next company, AI website + marketing automation).

Enterprise agents: Tasklet (connects to work APIs, runs continuously), Complir (compliance for physical goods across borders).

Second-wave coding infrastructure (Arga, Sazabi, Superset). Agent security (Silmaril). Physical AI / deep technical (9 Mothers, Dispatch). The “just another wrapper” companies are gone. This batch is infrastructure and hard problems.

#been thinking about this a lot lately and Satya nails it with humans plus AI together is what creates value which means owning your evals, private evals like I wrote last week is where the IP lives

add this must read post from the founder of inference provider Fireworks and you can see where the world is going and this is key if you click and read the post “The result keeps surprising people. On the tasks they care about most, a tuned open model can match frontier quality at a fraction of the cost. What this week made clear is that cost was never the most important question.”

#regarding intelligence, for those who got to try Anthropic’s Fable, it is pretty extraordinary - what’s key here is acknowledgement that there was a window but now it has long gone as amazing models continue to build yet more amazing models

#the frontier labs have to be ambitious - don’t worry, Claude Code is a research product Anthropic tells Cursor 🤦🏻♂️

#🤯 certainly the future - what timing and more incredible performance - Fable-level intel for 1/2 the price? who needs one lab when you can have many with one query?

#solving the memory wall problem for GPUs - more context means more memory needed and only so much high bandwidth memory paired with GPUs - we will continue to see new ways to cache and do smarter offloading to solve this

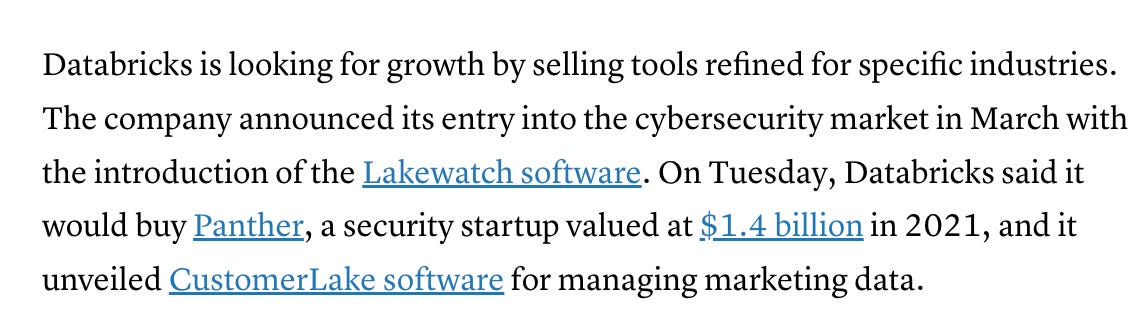

First huge congrats to What’s 🔥 reader Jack Naglieri of Panther, a leading AI SOC platform, which just sold to Databricks for $1.4B years after its last funding at a $1.4B valuation back in December 2021. You may say that is not an impressive valuation for a company valued at that price 5 years ago, but I would say it’s an insane exit to be able to grow into the ZIRP-era valuation and be relevant for today’s agentic world!

Congrats to Intercom as well - the poster child for how a founder comes back as CEO, goes founder mode, makes a big bet a few months after ChatGPT launch and 3 years later sold for $3.6B!