What’s 🔥 in Enterprise IT/VC #502

What a Long, Strange Trip It’s Been: SpaceX at $2 Trillion, Software in Limbo, and Venture in 2026

I had the Grateful Dead playing in the background this morning, and these lyrics from “Truckin’” made me think about today’s venture market:

Sometimes the light's all shinin' on me

Other times I can barely see

Lately it occurs to me

What a long, strange trip it's been

It’s truly an insane time as we have the largest IPO in history with SpaceX now worth more than $2 trillion, and the largest private company in the world, Anthropic, forced to take its newest models offline after the U.S. government restricted access. Meanwhile, the market is moving so fast and the uncertainty so high, software companies that would have been funded 12 months ago are having a hard time raising capital.

This is the startup market in June 2026.

At the top, the outcomes have never been bigger. Capital is flooding into frontier AI, chips, data centers, robotics, defense, energy, and space. For a handful of companies, the light has never shined brighter.

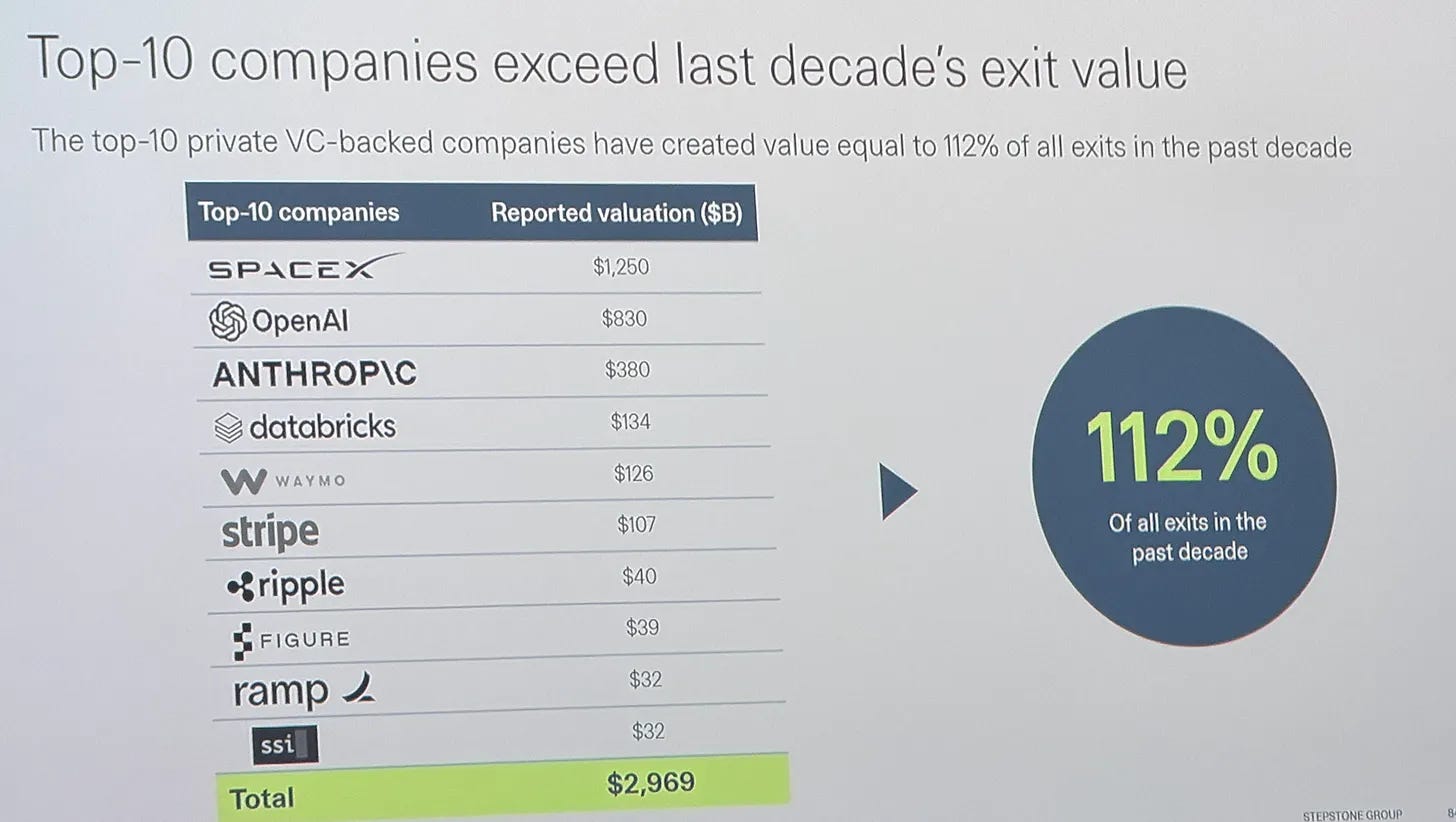

Earlier this year, one of our boldstart LPs, StepStone, shared this chart at its annual meeting. It captures just how concentrated venture has become: the top 10 private venture-backed companies represented 112% of the value of all venture exits over the prior decade.

And this was before SpaceX’s IPO and Anthropic’s recent rounds.

In fact, here is what it looks like now - thanks Fable.

Just two companies now represent more value than every venture-backed exit from the last decade combined 🤯. The concentration is simply staggering.

Hardware is simply easier for investors to underwrite right now. It’s physical and scarce, and building it requires enormous capital and deep technical expertise. For many VCs, software is much harder to underwrite but IMO that’s where the opportunity lies!

Every investor I talk to is asking some version of the same questions: What happens when the next model drops? Does the model provider absorb your product? Does your edge disappear overnight? If everyone can build software faster and cheaper, where does lasting value accrue?

It’s easier for many investors to do nothing and just wait until they see signs of a breakout or more of an inflection point. This means many companies with real customers and real revenue are struggling to raise because nobody can say with certainty what software will be worth in three years.

But I believe that uncertainty is exactly where some of the biggest opportunities will be built.

Look at what happened with Anthropic and Fable. Before government restrictions disrupted access, enterprises were already wrestling with rising token costs and limited control over how models could be used. Even Meta is reportedly moving to curb employee token usage as its internal AI costs climb. This is exactly why enterprises cannot rely on a single model provider.

As I’ve said repeatedly before (What’s 🔥 #500 and 501) the opportunity is in applications that work across multiple models, route workloads intelligently, protect proprietary data, manage costs, preserve institutional context, and keep running when a provider or policy changes underneath them. This is only going to accelerate with this latest government intervention - enterprises and founders need more control over their models and data.

Satya Nadella recently offered a framework that I think nails where the value is heading. He argued that a company’s private evals may ultimately become its most valuable IP. (h/t to Gokul for summarizing this)

What’s an eval? Think of it as your company’s custom exam for AI. Not a generic benchmark, but your specific test: Did the model approve the right refund, catch the compliance violation, prioritize the correct security alert, and complete the job at a cost that makes sense? Generic benchmarks tell you which model is smartest. A private eval tells you which model is best for your business. Satya’s test for control is simple: run your eval on model A, swap in model B, and see whether you can keep improving. If you can, you own the application. If you can’t, the model owns you.

Models may become interchangeable sources of raw intelligence, but your private eval captures something they don’t have: your proprietary definition of good, built from years of customer feedback, failures, edge cases, regulatory requirements, and expert judgment. The model supplies the intelligence; the eval defines what valuable intelligence means. And the eval isn’t the whole moat. The real defensibility comes from private evals combined with proprietary context, workflow integration, customer feedback, and execution data. Every completed workflow improves the eval, which improves the product, drives more usage, and generates more feedback. That compounding flywheel is a capability every AI-native startup, SaaS company, and enterprise will need.

This is also why I keep coming back to ROI per workflow as the metric that matters.

The eval measures whether the workflow works, while the software determines which model delivers the best outcome at the right price.

Hardware may be easier to underwrite because its barriers are visible. But software will own the context, evaluation, orchestration, and workflows that turn intelligence into enterprise value. That’s a massive opportunity, and much of the market is still too uncertain to see it.

So yes, this is one of the hardest times I can remember to raise money for a software company. But for the right software companies, hard to underwrite doesn’t mean the opportunity won’t be massive.

What a long, strange trip it’s been.

And somewhere inside all this uncertainty, enormous software companies are being built.

As always, 🙏🏼 for reading and please share with your friends and colleagues!

Scaling Startups

#love this…

#and this - Elon himself gave SpaceX less than a 10% chance of succeeding:

“I gave SpaceX less than a 10% chance of succeeding at all, to be clear. In fact, I told people this: I said, ‘look, we’re probably going to fail, but, you know, we should give it a try because if we don’t, if if there’s not a new company that enters space, we will never be a truly spacefaring civilization.’”

#there’s another one like this out there now!

Enterprise Tech

#🤯 Claude Fable 5 is out or Mythos for everyone but while super impressive, Anthropic also partially botched the release. First here’s what’s amazing: Felix talks about the third era of AI: I believe we're about to see a major shift, moving from giving AI tasks to giving it responsibilities.

#no longer…must read as the government now has shut down access to foreign countries and foreign nationals, given Anthropic can’t easily identify those it shut down pure access - i suspect this will be resolved by next week but the implications are massive and will only accelerate the idea of control your AI and data

and the view from other countries like India - here’s Zoho’s founder - open source = more control

#💯 before the government intervention, the Fable release and how it was done was already going to accelerate the need for more control of your AI

#btw, you don’t want to get on the Anthropic enterprise tier as its all token consumption

#🤔

#what OpenAI is thinking about cybersecurity with their new hire from Semgrep

#need more original data! Model collapse: AIs trained on AI outputs lose rare, creative “tails” of data first. Generations converge to bland, homogenized slop which is irreversible even with some human data mixed in.

#your data, your AI - Meta also moving from open source to closed and focusing on personal AI

#speaking of personal AI, not sure if I want Meta reading all my data though - look at this chart from Clem below, massive improvements!

#Brian from Coinbase nails it

#🎯 robotic model performance about to make some major step changes - watch Pete Florence from Generalist AI below

#in person experiences as the hedge against AI? It’s why the price of sports teams and other physical assets are going (FT)

#great read on Unitree, a word leader in developing robots

Markets

#just wanted to reshare this 🤯

#SaaS not dead for all, just for some