What's 🔥 in Enterprise IT/VC #300

What recession? If u can't sell dev tools now, it's not the market as 💰 is there

It was a huge 💪🏼 week for cloud earnings this past week.

New data from Synergy Research Group shows that Q2 enterprise spending on cloud infrastructure services approached the $55 billion mark. Despite turbulence in currency markets and a much strengthened US dollar, that still represents 29% growth from last year. Had exchange rates remained constant over the last year, the growth rate would have been around six percentage points higher. As spending on cloud services continues to rise inexorably…

In other words, the cloud grew 35% YoY in constant currency. If you’re a devtools founder, there is no better sign for what’s ahead than Satya’s comments around Microsoft’s continued growth in cloud, containers, and Kubernetes (Azure Arc).

Organizations in every industry continue to choose our cloud to align their IT investments with demand. We are seeing larger and longer-term commitments and won a record number of $100 million-plus and $1 billion-plus deals this quarter.

More public cloud spend means more new applications being built and deployed leading to more spend on dev tools, orchestration, security and more…which Satya highlights here.

So I think that we'll do fine there. The other one is also people building new applications at a completely new frontier. I mean, there are two numbers that I talked about. One is the triple-digit growth in Cosmos DB and triple-digit growth in container app services.

You take those two things and you say, what are people doing? People are writing applications at a completely different frontier of efficiency, which is cloud-native serverless container-based types of applications. And so to me, that's another way for you to make sure that your IT spend goes a long way in a time like this.

Founders, don’t tell me recession - enterprises are continuing to aggressively build and deploy new cloud-based applications and Microsoft, despite slowing YoY growth in Azure, reiterated its forecast for a strong Q3.

Bill McDermott from ServiceNow summed it up nicely from his earnings call:

“The secular digital transformation tailwinds are blowing stronger than the macro crosswinds.”

If you can’t get users to use and convert to buyers, then I’d say you have bigger problems like taking another look at your value proposition and product. But whatever it is, don’t tell me you can’t sell because it’s a recession whether you technically believe the definition or not 😃. Yes, I know, some of this is large cap growth due to vendor consolidation around an OK product but it’s still on you to build an amazing 🪄 product as the 💰 is there.

I’d also add that it looks like these companies are still quite bullish about the future. as many are continuing to ramp sales and marketing 2-4 quarters in advance. Also notice how many are infrastructure companies. Once again, enterprises building new apps and deploying to the cloud equals more spend for devtools, infra, and cybersecurity to lock it all down.

Going back to Bill McDermott, here’s more on the durability of enterprise software growth.

The secular digital transformation tailwinds are blowing stronger than the macro crosswinds. ServiceNow generates an unmatched combination of organic growth and profitability at scale. We believe there is a generational value creation opportunity here on every level of our company. Therefore, we are hiring, expanding and investing for the future.

Growth companies don't get stronger than this one. Before I hand things over to Gina, let me offer some additional color to underscore the state of the business. Enterprise software is an all-weather industry. Some businesses out there are prioritizing enhanced productivity to lower costs.

Others are evolving business models to stimulate growth. All of them know full well that digital technology is the only answer. That's why the demand environment to software is consistent and durable. Market research from IDC and several prestigious institutions on this call, I might add, have all affirmed the stability of technology budgets.

Yes, I’m long term bullish on the future but note there are two headwinds for startups:

According to Bill, “We’re going to see some longer sales cycles” given the uncertainty of the economy.

In times of cost cutting, usually more 💰 goes to large incumbents as spend gets consolidated so startup vendors better have an amazing, not just a good, product to offset the distribution advantages of LargeCo

As always, 🙏🏼 for reading and please share with your friends and colleagues.

Scaling Startups

💯 🧵

Gokul Rajaram@gokulrEarly stage B2B Founders: If you have to choose between one very large first customer (say $500k+ ACV) and ten smaller first customers (say $50k ACV each), the right choice (at least for venture funded companies) in most cases is the latter. Why?2:22 AM · Jul 29, 202284 Reposts · 712 Likes

Gokul Rajaram@gokulrEarly stage B2B Founders: If you have to choose between one very large first customer (say $500k+ ACV) and ten smaller first customers (say $50k ACV each), the right choice (at least for venture funded companies) in most cases is the latter. Why?2:22 AM · Jul 29, 202284 Reposts · 712 LikesNot only just for consumers but applies to PLG enterprise and dev first cos

Lenny Rachitsky@lennysanI've just published a completely revamped playbook for finding your first 1,000 users. This is based on researching 100+ B2C startups, talking to 30+ founders, and collecting tons of never before shared stories. This is def my new favorite post I've written. *Read on* 3:13 PM · Jul 26, 2022240 Reposts · 1.59K Likes

3:13 PM · Jul 26, 2022240 Reposts · 1.59K LikesOn VCs and valuation…takes awhile for public valuations to trickle down to seed. In a normalized world, founders raising seed need to think about what will my A round look like if I price myself on markets 2 years ago.

Howard Lindzon@howardlindzonI continue to be shocked by very high valuations I see at seed stage - my day job for 16 years. I am reminded of line from 'War Games' today when I think about seed investing... “A strange game. The only winning move is not to play.” I10:48 PM · Jul 26, 20229 Reposts · 174 Likes💯 and many times longer for dev tools and infrastructure cos…

Paul Graham@paulgStartups usually take a while (often a year or two) to figure out exactly what their business is. The biggest preventable cause of failure is spending too much money, by hiring too many people, during this period.6:40 PM · Jul 24, 2022681 Reposts · 5.13K Likes

Enterprise Tech

Momentum Cybersecurity report is out 1st half 2022 , includes data on investment, M&A, and market trends like Gartner Top 7 cyber risks

The holy grail for developers and companies - developer speed and self service with centralized governance

Sid Palas@sidpalasDevOps is dead 💀, long live Platform Engineering! 1) Developers don't like dealing with infra 2) Companies need control of their infra as they grow Platform Engineering (and Internal Developer Platforms) enable these two facts to coexist. Here's how: (1/n)2:25 PM · Jul 26, 2022363 Reposts · 1.82K LikesGreat 🧵 + comments on local vs. cloud developer tooling…

Erik Bernhardsson@bernhardssonIn the long run, I expect most/all of developers doing things locally will go away. Developing, testing, building, running, deploying, etc. When developers need to run things locally today it’s a sign that cloud tools aren’t there yet imo.4:22 PM · Jul 24, 202221 Reposts · 446 LikesDo data-driven companies actually win by Benn Stencil, founder of Mode Analytics - great post on power of data and how moat builds over time and important for early stage founders to not put too much faith in data driven decisions at beginning

That’s why I’m skeptical of MTRX. Companies, especially young ones, that orient themselves around data can often put too much faith in its magical transformative powers—sometimes to disastrous effect. That’s not how it works. Data is a competitive edge, but it’s earned, from months and years of grinding at the table, counting cards, playing hand after hand, slowly bringing down the house.

In other words, don’t do this…

Eric Zhu in SF 🌁@ericzhu105Me pulling up google analytics to track the 1 active user on my startup's landing page 8:53 PM · Jul 29, 2022122 Reposts · 2.18K Likes

8:53 PM · Jul 29, 2022122 Reposts · 2.18K LikesOn accelerating sales cycles from Jake Stein, co-founder of CommonPaper and previously RJMetrics and Stitch Data (sold to Talend) and here’s the punchline:

Standard Contracts Accelerate Sales Cycles

At my last company, Stitch, our sales cycle was between three and four months long. 25 – 50% of that time was spent on contracting. The biggest lever we had for speeding up contracting was increasing the proportion of deals on our contract template rather than on our customer’s.

Common Paper users have found that using standard agreements allows them to reduce the proportion of deals on customer paper by 48%. If you’d like to use standard contracts to accelerate your sales cycles, try Common Paper for free.

Jake Stein@jakesteinFaster sales cycles are magic. They allow you to increase customer acquisition spend without decreasing runway, even if win rate, acquisition cost, ACV, and starting capital are constant. I wrote a post about how and share a model you can customize: commonpaper.com/blog/impact-of… 3:44 PM · Jul 26, 20227 Reposts · 5 Likes

3:44 PM · Jul 26, 20227 Reposts · 5 LikesEdge ML is early and real and needs an easier way for enterprises to deploy and scale. Huge congrats to Wallaroo, a portfolio co, on bringing edge to space 🚀, yes space - here’s some commentary from Vid Jain, founder of Wallaroo and an article from TechRepublic

And this is why edge ML deployment has become so important. In fact, over 40% of our current pipeline involves the edge, spanning industries like manufacturing, telecommunications, automotive, energy & utilities, logistics, and travel & hospitality. The models can be built anywhere, but in order to generate value they need to be deployed at the edge, due to latency requirements measured in milliseconds or else due to environments with limited/no connectivity like gas pipeline or oil derricks far from broadband.

This is part of why I believe we are seeing accelerating growth at Wallaroo as a Series A startup competing with cloud and SaaS giants.

What’s 🔥 in Europe and why we at boldstart are bullish on dev first and PLG founders across the pond

Ed Sim@edsim💯❤️ this from my partner @shomikghosh21 - 12 day one investments in Europe @Boldstartvc over the years and look forward to partnering with more with dev first founders Shomik Ghosh 🇺🇦 @shomikghosh21Snack Bites #40: Euro Trip! - A quick post on how the European enterprise software ecosystem is popping! - How constraints lead to success - Why so many Euro B2B companies are PLG first Thanks to all the amazing people who hung out with us on this trip! https://t.co/FGYcEsSCqP12:33 PM · Jul 27, 20224 Likes

Shomik Ghosh 🇺🇦 @shomikghosh21Snack Bites #40: Euro Trip! - A quick post on how the European enterprise software ecosystem is popping! - How constraints lead to success - Why so many Euro B2B companies are PLG first Thanks to all the amazing people who hung out with us on this trip! https://t.co/FGYcEsSCqP12:33 PM · Jul 27, 20224 Likes😲 Still big funding for new Layer 1 networks - Aptos, ex Facebook Diem crypto team, raised a $150M Series A at an over $2B valuation

Aptos@AptosLabs1/ Today, we announced our $150M Series A funding round. This is a testament to our team's technical expertise, the strength & activity of our ecosystem and the vision & ethos we all share.medium.comEntering The Next Phase of The Aptos Journey With Added Funding and New Partners 1:27 PM · Jul 25, 2022256 Reposts · 1.15K Likes

1:27 PM · Jul 25, 2022256 Reposts · 1.15K Likes😲 Retool, a low code no code platform for building internal tools just raised at a $3.2B valuation! And launched a new free plan…while there are lots of companies going after this space, Retool has simply had killer execution

Retool@retoolAt Retool, we’re building a new way to create software—the only way to experience it is by trying it out! So, we’re launching a new free plan. Developers and small teams of up to 5 can now build unlimited apps for free. Learn more and sign up:retool.comIntroducing our new free plan 1:07 PM · Jul 28, 202219 Reposts · 79 Likes

1:07 PM · Jul 28, 202219 Reposts · 79 Likes

Markets

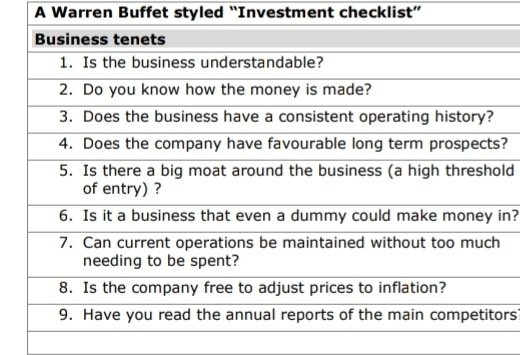

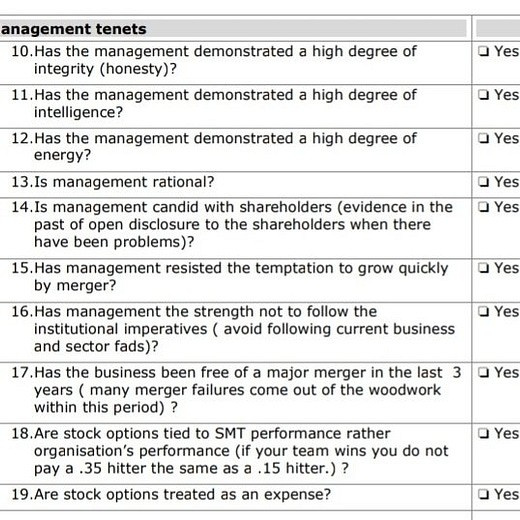

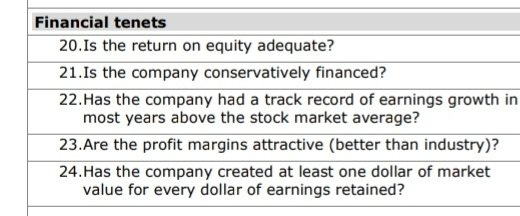

In this market many folks going back to basics - here’s Warren Buffet’s checklist

Compounding Quality@QCompoundingThe investment checklist of Warren Buffett:

1:39 PM · Jul 28, 2022219 Reposts · 859 Likes

1:39 PM · Jul 28, 2022219 Reposts · 859 Likes